If there is one clear takeaway from recent industry conversations and conferences, it is this: No one is fully ready for the “AI revolution.”

Even the so-called “haves” with massive engineering teams and virtually unlimited capital are cautious. Large technology companies are investing heavily in AI initiatives, yet they openly acknowledge the operational, governance, security, and reliability challenges involved. If organizations with thousands of engineers are still working through these issues, all finance and IT leaders should approach adoption with discipline and humility.

From the CFO seat, this changes the framing. The question is not what 2026 will look like. The more useful question is:

How do we responsibly roll out AI in finance in a way that strengthens control, improves accuracy rather than undermines it, and does so at a predictable cost with positive ROI?

In conversations we have every day with finance and accounting leaders, this is the theme that consistently surfaces. There is interest. There is curiosity. There is pressure—especially given rapid adoption in other areas such as engineering. There is far less clarity on how to operationalize AI without increasing risk and taking a step backward in the accuracy and transparency of financial reporting.

Here are our top seven considerations for a responsible AI rollout in finance.

1. Start With Governance, Not Tools

Before discussing vendors, models, or pilots, finance leadership must address governance.

AI initiatives introduce new questions:

- How are outputs validated?

- Where is data stored and processed?

- How are models monitored over time?

- How are they incorporated into SOC controls and audit procedures?

- What does “human-in-the-loop” really mean?

Many organizations are experimenting at the edge of policy rather than inside it. That is not sustainable for a regulated finance function.

Research from organizations such as NIST, McKinsey, and MIT Sloan reinforces that trust, explainability, and governance are the primary barriers to enterprise AI adoption. For CFOs, those barriers are not abstract concerns. They directly affect auditability, control environments, and board-level risk exposure.

AI in finance must be deployed within a clear governance framework. Without that, any speed gains from AI simply magnify the risk.

2. Accept That Build vs. Buy Is Evolving

Historically, finance technology decisions often centered on a build versus buy debate. That distinction is becoming less meaningful in the AI era. Every day, we see a finance executive touting how proud they are of a bespoke application they’ve built. But once the headline fades, what is the reality?

There is no doubt that the power of AI is here to stay. Over the past several decades, other technologies such as the internet, mobile, and the cloud have enabled new capabilities. But are these technologies used in a “one-off” manner by businesses? Perhaps, initially, they were. Over time, precisely because of their power, these technologies started to be commonly provided by third-party application providers that can be centrally managed.

Bespoke solutions may solve a narrow use case, but they rarely scale and don’t age well. Maintaining internally built AI tools raises practical challenges:

- Ongoing model tuning and monitoring

- Documentation and explainability requirements

- Inclusion in SOC testing and internal controls

- Overall higher cost of ownership

- Security reviews and access management

Even organizations with substantial engineering resources are acknowledging that fully custom AI builds are difficult to maintain outside of narrow, corner-case applications. And even these corner-case applications create complexity for security teams, which reduces control and increases risk.

What is emerging instead is an architectural approach. Rather than building everything or buying disconnected point tools, finance teams need a coherent AI architecture that:

✔️ Embeds governance and security from the start and maintains these over time

✔️ Integrates with existing systems of record

✔️ Scales across use cases without multiplying risk

This architectural mindset will increasingly replace simplistic build-versus-buy conversations.

3. Focus AI Where Control Already Exists

Public research from firms such as Gartner and Deloitte shows that most finance organizations are piloting AI in limited, well-defined workflows rather than deploying it broadly across core accounting processes.

This approach is prudent.

In finance, early traction is showing up in areas where:

- Processes are repeatable

- Risk is well understood

- Human review remains embedded in the workflow

Common starting points include:

- General Ledger operations

- Close management and reconciliations

- Procure-to-pay workflows

These areas already operate within structured controls. AI can augment productivity without replacing accountability. And frankly, many of them are already automated to a great extent. The benefit of AI systems here is that these activities are completed in real-time or near-real-time.

From a CFO standpoint, every pilot must answer simple questions:

Does this improve output quality or speed while preserving control and auditability?

Do I need these activities done in real time?

If the answer is uncertain, given resources for most organizations are limited, the project will likely not be prioritized.

4. Close Management as a Responsible Starting Point

Across industries, the close remains slower and more manual than it should be. Many organizations still operate with a 10- to 12-day close driven by manual coordination and spreadsheet-based reconciliations.

Benchmarks from APQC and the Hackett Group show that top-performing finance teams close several days faster than peers while reporting fewer post-close adjustments. Moving toward a 5- to 7-day close is increasingly achievable when task orchestration, reconciliation tracking, and exception visibility are systematized.

Close management represents a responsible entry point for AI and automation because it improves:

- Transparency

- Task accountability

- Exception detection

- Documentation consistency

The outcome is not only speed, but also earlier confidence in the numbers that feed forecasting, executive reporting, and board materials.

Given the persistent accounting talent shortages and wage pressure reported by the AICPA and the U.S. Bureau of Labor Statistics, it is a practical necessity to enable existing teams to scale output without proportional headcount growth.

At the same time, most financial data still originates in ERP systems, which remain the system of record for transactions, subledgers, and financial reporting. As ERP vendors begin embedding AI capabilities of their own, finance leaders will need to consider how those innovations interact with the close process itself.

Whether AI capabilities emerge primarily within ERP platforms or through specialized solutions, the real opportunity lies in connecting these layers so that data, workflow, and intelligence operate together. When that alignment occurs, the close becomes not just faster, but structurally more reliable and scalable.

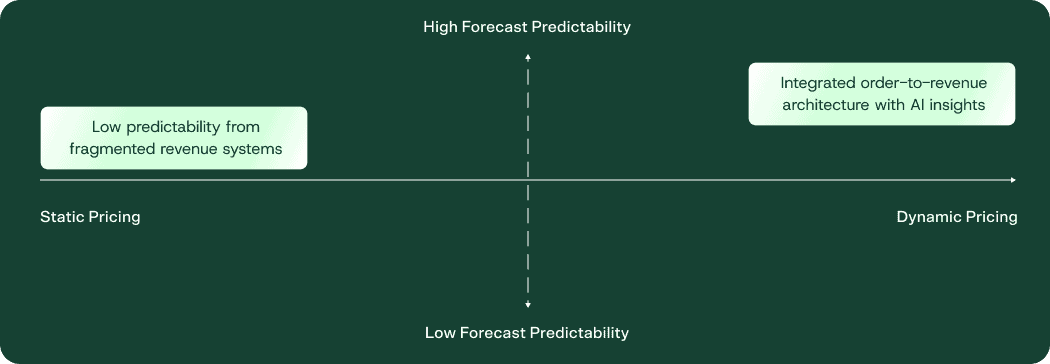

5. Revenue Complexity Requires Architectural Discipline

Industry surveys from OpenView and SaaS Capital show continued growth in usage-based and hybrid pricing models. As pricing flexibility increases, revenue volatility and forecasting complexity increase as well.

Public CFO surveys from PwC, EY, and Deloitte consistently rank forecast accuracy and cash visibility among top priorities. These expectations do not diminish when pricing models become more dynamic.

This environment demands integrated order-to-revenue architecture. CPQ, billing, and revenue recognition systems must support flexibility without repeated reimplementation or manual workarounds.

Without architectural discipline, AI layered on top of fragmented revenue systems will amplify inconsistencies rather than resolve them. At any reasonable level of scale and complexity, system speed and AI processing cost become larger concerns—and ones that are not often discussed. CFOs, especially those dealing with more revenue complexity, must consider how additional AI layers might impact their architecture.

6. Cybersecurity and Trust Are Not Secondary Concerns

Board-level surveys consistently rank cybersecurity among the top enterprise risks. The introduction of AI-driven tools and agents heightens these concerns.

Data leakage, access control gaps, and unclear accountability for model outputs are among the primary inhibitors to enterprise-scale AI adoption in regulated environments. Both APIs and the MCP are a traditional cyber attack vector, making it safer to leave these to third-party providers who have full teams of people maintaining them.

Finance leaders should assume that enterprise and government adoption will move more slowly than market hype suggests. Trust frameworks, standards, and testing protocols must mature before widespread deployment becomes acceptable.

The trajectory resembles early cloud adoption. Over time, standards emerged and trust increased. AI will follow a similar path, but governance will determine the pace.

7. Manage Expectations Around the AI Narrative

One uncomfortable observation is that broad enthusiasm for the AI revolution is not evenly distributed.

Many finance leaders feel pressure to act, yet remain unconvinced that current tools justify sweeping transformation. The most visible beneficiaries of the hype cycle are often engineering teams, investors and early movers, not operational finance teams responsible for accurate reporting.

This tension reinforces the need for a trusted advisor mindset. Finance does not need to chase headlines; it needs to implement change in a way that prioritizes the preservation of reliability.

Responsible AI deployment in finance means:

- Clear governance

- Controlled pilots

- Architectural alignment

- Explicit accountability

What the Data Shows

Across public research and industry benchmarks, several consistent patterns emerge:

- AI adoption in finance is early-stage and deliberate, with most organizations piloting limited use cases rather than deploying AI broadly across core accounting processes. (Gartner, Deloitte)¹

- Faster month-end close correlates with stronger financial control, as top-performing finance teams close days faster than peers while reporting fewer late adjustments. (APQC, Hackett Group)²

- Forecast accuracy and cash visibility remain top CFO priorities across economic cycles. (PwC, EY, Deloitte)³

- Usage-based and hybrid pricing models are becoming more common, increasing revenue volatility and forecasting complexity. (OpenView, SaaS Capital)⁴

- Trust, context, and explainability are gating factors for enterprise AI adoption in regulated environments. (NIST, McKinsey, MIT Sloan)⁵

These findings reinforce a practical conclusion: AI in finance should be introduced in ways that strengthen control, visibility, and predictability.

Final Perspective

The finance function needs discipline—especially when adopting powerful new technologies.

AI will continue to evolve. Vendor claims will continue to expand. Market narratives will continue to accelerate.

From the CFO perspective, the mandate is steady: Protect the integrity of financial reporting, responsibly allocate capital, improve visibility, and introduce innovation without weakening controls.

Responsible rollout, grounded in governance and architecture, will define successful AI adoption in finance far more than speed alone.