Determining the standalone selling price (SSP) is rarely straightforward and requires accountants and finance leaders to apply judgment and expertise beyond simple number-crunching. The methods for determining the individual selling price of each good and service offered within a multi-element contract (irrespective of bundles, discounts, and other deal-making adjustments) all involve making judgments after conducting thorough analysis and reviewing internal documentation.

Manually conducting annual (or more frequent) research and calculations bogs down accounting teams. Completing this requisite effort to comply with Generally Accepted Accounting Principles (GAAP) and ASC 606 or IFRS 15 often causes accounting staff to spend months or even entire quarters performing manual SSP analysis.

Understanding SSP Under ASC 606 Revenue Recognition

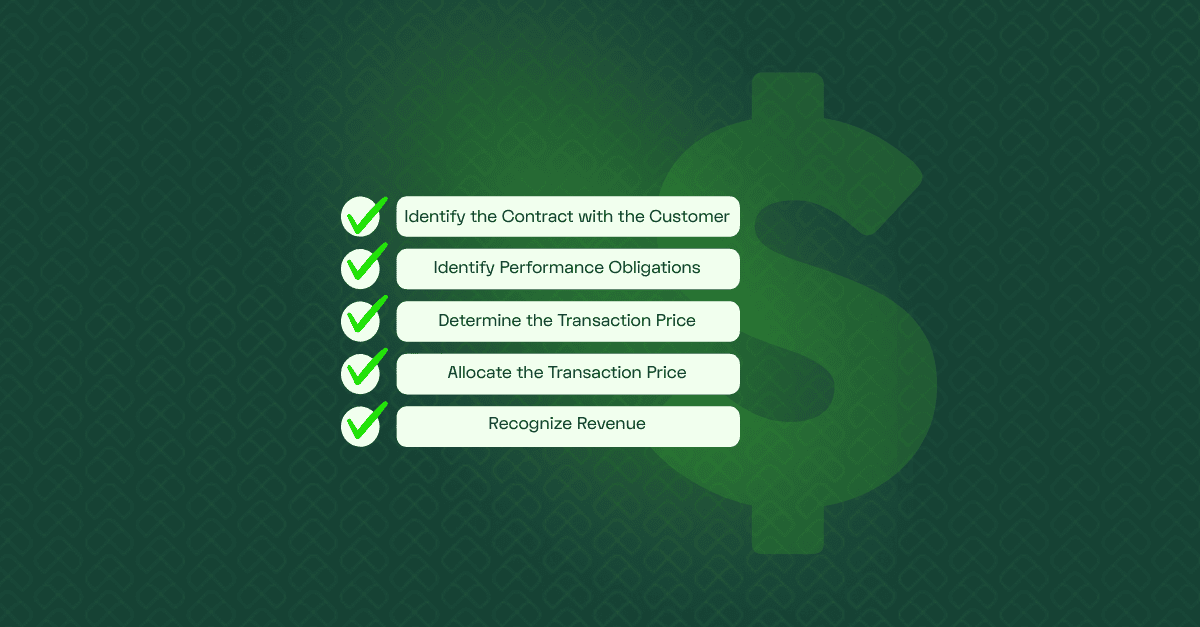

ASC 606 is the five-step accounting standard guiding revenue recognition for companies operating in the US. As part of its requirements, revenue accounting practices for multi-element contracts must proportionally allocate the total of revenue that will be earned via any contract to each of the contract’s elements.

For a quick refresher regarding ‘what is SSP? ’, it’s crucial to know the following terms related to SSPs:

- Standalone selling price: This refers to the default price for a good or service if sold independently, without any adjustments that incentivize a sale or finalize contract negotiations.

- Performance obligations: Each contractually promised good or service to be delivered to a customer counts as its own, separate performance obligation.

- Transaction price: The transaction price is the total, contractually agreed-upon value a customer pays, whether or not the contract involves multiple elements or performance obligations. Effectively, it is the aggregate standalone selling price of all components.

- Allocation: With each contract finalized, the transaction price must be segmented and the revenue allocated to each performance obligation according to its SSPs.

SSPs can be considered ‘observable’ if a given good or service is already sold separately by the business. However, if those elements are normally sold as part of a bundle instead of individually, there may not be an existing, observable SSP. In these and similar cases, accountants must estimate the SSPs.

Further complicating these judgments, sales staff often give non-uniform discounts (e.g., a flat percentage off the transaction price, free onboarding services, free support for a year). Sales might also pursue multi-year deals that could lock in pricing or bring in considerable amounts of deferred revenue, which must be recognized over time.

SSP Estimation Methods

When businesses need estimated standalone selling prices for contracts containing multiple performance obligations, they typically utilize one of three methods:

- Adjusted market assessment approach: Derive SSP by considering the broader market data and competitors’ pricing strategies for the goods and services in question, then modify the value according to factors like market position, revenue model, and brand recognition and reputation. The adjusted market assessment approach likely involves the most outside research.

- Expected cost plus margin approach: Starting from a COGS or similar calculation, determine what standalone selling price will account for production expenses and operating costs before adding a decent profit margin to reach the price; typically 10% gets touted as being an appropriate margin, but this figure varies significantly by industry, and some market research is likely necessary.

- Residual approach: As a last resort, remove all known or observable standalone selling prices from the contract’s total transaction price. What’s left, or the ‘residual,’ then comprises the remaining, relative standalone selling price(s).

In practice, the “best” method is the one you can defend with data and apply consistently. Start with the strongest evidence you have (observable prices or solid cost models), use market inputs to sanity-check results, and reserve the residual approach for truly variable or novel offerings.

Whichever path you take, document your assumptions, monitor them against actuals, and revisit SSPs as market conditions, pricing strategies, and your product mix evolve so revenue stays accurate, auditable, and aligned with the economics of the deal.

Why SSP Revenue Recognition Matters

Per ASC 606, the fourth step of proper, compliant, and accurate revenue recognition involves allocating portions of a contract’s transaction price to each of the performance obligations included within it. Put simply, the revenue a company earns must be traceable to each of the goods and services exchanged for it.

However, this isn’t just a straightforward, technical accounting policy or practice; the SSPs informing revenue allocations must consider numerous factors.

These include:

- Market analysis

- Historical prices

- The cost of goods sold (COGS)

- Bundle compositions

Moreover, while best practices suggest evaluating SSPs annually, some industries or market fluctuations may require a business to reassess its SSPs every quarter.

The research, documentation, and frequency required to determine an SSP remain significant because these judgments will be scrutinized, at a minimum, by compliance auditors, reviewers from the Securities and Exchange Commission (SEC), and internal stakeholders.

Yet, despite the high stakes, too many accountants still make SSP judgments while working across spreadsheet after spreadsheet to gather needed information. It’s an approach that only invites delays, mistakes, and data entry errors.

Comparatively, teams that streamline SSP calculations and revenue allocation with automated historical analysis save weeks and months of time while remaining compliant with ASC 606.

Manual SSP Processes and Financial Reporting Risks

Determining standalone selling prices (SSPs) manually is one of the most tedious and high-stakes responsibilities a revenue accountant faces. The process demands hours spent chasing data across spreadsheets, reconciling inconsistencies, and documenting every assumption to satisfy audit requirements.

Each step, from gathering historical transactions to calculating SSP ranges, requires painstaking attention to detail, yet still leaves room for error and second-guessing. Accountants often find themselves double-checking formulas late into the night or revalidating prior-period logic just to maintain compliance. It’s exhausting and inefficient.

Manual SSP management traps skilled accounting professionals in administrative tasks that add little strategic value while increasing the likelihood of calculation errors, version drift, and audit findings. By contrast, an automated system that continuously analyzes historical data, applies consistent allocation logic, and updates SSPs in real time transforms the process entirely.

Instead of reactive firefighting, accountants can focus on oversight, exception handling, and forward-looking analysis. Automation restores confidence in financial accuracy, strengthens audit readiness, and gives finance teams back the time to actually drive the business forward.

How SSP Automation Simplifies Revenue Recognition and Transaction Price Allocation

Using a tool that automatically analyzes historical data to determine SSP significantly improves the accuracy and defensibility of the standalone selling price according to ASC 606. With automation, accountants spend less time wrangling spreadsheets and analyzing years of data.

With a tool like RightRev, SSP automation will also apply policy-driven discounts and account for variable considerations (i.e., contractually stated price fluctuations based on future events or conditions). Per ASC 606, discounts that aren’t specific to certain performance obligations must be applied evenly across the contract’s elements according to the proportional breakdown of their SSPs.

Moreover, by automating SSP and revenue recognition processes, a business logs all activity and enables continuous SSP reassessment over time. This facilitates the enforcement and recalculation of SSPs upon contract renewals or following contract amendments and modifications.

Changes are documented, and there is potential to require approval from specific roles. By capturing all this activity in an audit trail, businesses not only operate in compliance with ASC 606 but also gain confidence in their auditability.

Key Data for Determining SSP and Allocation

Businesses looking to automate SSP determinations and revenue allocations must prioritize clean, consistent data across critical inputs. Formatting (e.g., including two decimal places for cent calculations) must be uniform across the associated fields, or a system will interpret the values as distinct or unrelated when performing automations.

Critical inputs include:

- Product hierarchies or tiers

- SKUs

- Price lists

- CRM fields

- CPQ fields

- Billing events

- Finance policies

Treat these as a system, not a checklist. Align taxonomies across teams (product↔CRM↔CPQ), define a single source of truth for each field, and enforce data quality rules at ingestion.

Add ownership, change controls, and an audit trail so when prices, SKUs, or policies shift, your SSP logic updates predictably, and finance can trust every number that rolls up to revenue.

Handling Common Real-World Scenarios

Consider the following scenarios involving automation and how these capabilities significantly alleviate the accounting and finance teams:

- Bundled software and services: Contract elements are segmented according to observable SSPs, with the automation handling corresponding allocations as revenue is recognized.

- Product tiers and ramps: Whether discounts are applied consistently or at varying rates based on quantities purchased or other factors, an automated system enforces these rules across the contract or as different thresholds are met, respectively.

- Usage-based pricing: Similar to product ramps that apply different discount amounts at different thresholds, an automation integrated with consumption metering will use dynamic pricing models (and recalculations) appropriately and as configured.

- Multi-year deals: Rules configurations allow automations to segment a contract into individual years, simplifying ASC 606 regulatory compliance.

The thread through all of these is control at scale. When allocation, discount logic, consumption metering, and term segmentation run from the same rules engine, you cut manual effort, shrink error risk, and produce revenue schedules that are consistent, explainable, and audit-ready.

The payoff isn’t just speed to close; it’s confidence that every bundled deal, tiered price, usage spike, and multi-year ramp flows into GAAP-compliant revenue the same way, every time.

Handling Contract Modifications and SSP Updates

Contract modifications introduce significant complexity to revenue recognition, and to standalone selling price (SSP) usage in particular:

- If the modification is a separate contract (e.g., adding distinct goods/services at their current standalone price), the original contract’s allocation stays as is. The new items are allocated using their SSPs at the modification date; you don’t revisit the original allocation.

- If the modification is not a separate contract (e.g., adds/removes/changes remaining performance obligations in the current contract):

- You update the transaction price and reallocate it to the remaining performance obligations using SSPs at the modification date (not the inception-date SSPs).

- Any impact on satisfied performance obligations is recorded as a cumulative catch-up (if applicable), while unsatisfied obligations are recognized prospectively based on the new allocation.

- A cancellation or significant scope/price change that’s accounted for as a termination and new contract is treated similarly: use current-date SSPs for what remains.

- SSP itself doesn’t “change” because of discounts or concessions; those are part of the transaction price. But your allocation uses SSPs (inception-date SSPs for untouched, separate contracts; current-date SSPs for modified remaining obligations), which is why modifications can shift revenue timing even when list prices haven’t moved.

With automation, these remeasurements, recomputing SSP-based allocations, booking cumulative catch-ups, and updating schedules, are performed immediately and consistently, whether the entire multi-element contract is affected or only one element changes.

Practical expedients (approved shortcuts) can be configured; for example, SSP estimation policies (adjusted market assessment, expected cost plus margin, or residual approach where appropriate) and periodic SSP “locks” within a fiscal cycle, if allowed by policy. Whatever expedients you adopt must be applied consistently and disclosed in accordance with policy.

Let’s go over an example to put this into perspective.

A customer prepays for a one-year subscription, which is recognized monthly.

Mid-year, they upgrade to a higher tier and add a training package:

- If the upgrade and training are priced at current standalone rates → treat as a separate contract; allocate the new consideration using current SSPs; the original schedule continues unchanged.

- If the change modifies remaining obligations in the original contract → reallocate the remaining consideration to the remaining services using current-date SSPs and record any necessary catch-up.

In short, SSP is the anchor in a modification: You reassess it at the modification date for the remaining obligations, reallocate accordingly, and book any catch-ups consistently and transparently. Getting that right (and automating it) turns modifications from a risk into a routine step that’s defensible to auditors and predictable for the business.

Efficiency, Controls, Audit Readiness, and Reporting

Automating SSP and revenue recognition helps accounting teams reclaim significant hours that can be refocused on strategic financial tasks.

However, automation provides the additional benefit of audit readiness via more thorough audit trails and compliance reporting. To start, a business maintains confidence that its policies are enforced uniformly, with any deviations requiring appropriate approval (e.g., to maintain SOX compliance).

Should auditors investigate a business relying on automations, it’s simple to immediately highlight SSP determination methods along with their ranges and exceptions. The activity logs and audit trails supporting these capabilities also provide financial statement and disclosure support, providing data used to understand current operations and to forecast future strategies.

SSP Automation Implementation Playbook

Automation implementations generally proceed according to the following phases:

- Phase 1: Catalog and policy design: The process begins with creating a product catalog and determining the policies that will be enacted to enforce consistent, compliant SSP automations and revenue recognition. This includes deciding which method for calculating SSP will be used.

- Phase 2: Data readiness: All data relevant to the automations must be reviewed and prepared (e.g., uniform formatting, correcting any typos). This includes all data relevant to revenue recognition practices, such as SKUs, pricing, and data from CRM and CPQ solutions.

- Phase 3: Rule configuration and testing: After preparing the data, it’s time to configure the rules that the automation(s) will adhere to and that enforce the policies determined in Phase 1. This should involve repeated testing to verify that the configured rules operate as intended.

- Phase 4: Parallel run and variance analysis: Before going live with the automation, testing should include a ‘parallel run’ (i.e., performing prior SSP and revenue recognition processes while executing the automation). The results, assessed comparatively and via variance analysis (i.e., examining differences between expected and actual results), will inform the final adjustments to rule configurations.

- Phase 5: Go live and periodically refresh: Once this process is complete, the automation can be rolled out to (the joy of) accounting and finance teams. Sophisticated SSP and revenue recognition automations can self-adjust over time, depending on the configured rules and available historical data. However, it remains crucial to periodically (e.g., annually, quarterly) revisit this process and update product catalogs, realign policies, confirm data integrity and preparation, check rule configurations, and perform parallel runs and analysis.

Treat the phases as a living control framework, not a one-and-done project plan. Each cycle hardens your catalog, improves data hygiene, and sharpens rules so variances shrink and explanations get faster.

Pair that cadence with clear ownership and change controls, and “go live” becomes the start of continuous assurance: A system that adapts with your products and pricing while keeping revenue recognition predictable, auditable, and defensible.

Mini Case Example of SSP Automation

Consider a SaaS company in the software industry that sells software licenses for Product A on a subscription basis, meters highly variable consumption for Product B, and provides professional services (e.g., onboarding, configuration, maintenance) that lack a list price. Although a contract contains three separate performance obligations, the sales staff provides a single price for the bundle, and the customer purchases them collectively.

Manually performing the SSP and revenue recognition calculations for every month-end close takes considerable time and effort, which could be eliminated through automation.

With centralized SSP rules, automations easily determine SSPs by factoring historical data and proportionally breaking down the contract’s transaction price.

In this example:

- Product A would have an annual subscription divided into monthly payments. The software demonstrates standalone sales, so it has an easily observed SSP that’s distinguishable from the rest of the bundle by subscription pricing and the associated software license performance obligation.

- Product B would take monitored consumption data and the usage pricing (acting as the SSP) to determine how much revenue was earned each month from this stream.

- The ad hoc professional services could be determined using the residual amount of the contract price after accounting for Products A and B.

And, as performance obligations are met and revenue is recognized, the automation accordingly allocates that revenue. Not only do accounting and finance teams suffer little to no additional workloads, but they also accelerate month-end closing.

In turn, strategic decision-makers can access this data sooner and with fewer concerns regarding future corrections, enabling better forecast clarity. Moreover, the automations’ uniform, logged execution helps ensure ASC 606 compliance with audit trails as proof.

Automate SSP Without the Analysis Drag

Accountants and finance teams are still determining SSPs and recognizing revenue, wrestling with manual processes and spreadsheets, which only makes things harder for themselves. Automation accelerates and standardizes the process, while also improving audit readiness and forecast clarity.To learn more about RightRev’s leading revenue recognition automation, take a look at our SSP eBook or book 30 minutes with our experts to discuss ROI templates and audit-ready logs.