XaaS Lessor Accounting for Hybrid Hardware and Service Contracts

If you are a hardware company transitioning to a “Device-as-a-Service” (DaaS), or “Everything-as a service model XaaS, you have likely discovered a painful accounting truth: The economics of your business have fundamentally transformed. What used to be “hardware revenue” is now a hybrid contract with multiple performance obligations governed by different accounting standards. This shift places XaaS lease accounting at the center of revenue accuracy, compliance, and financial reporting.

For years, the lease accounting software market has been dominated by solutions built for lessees, i.e. the party recording the liability. Since the vast majority of companies in a lease agreement are equipment operators rather than equipment providers, lease accounting vendors optimized their solutions to bring operating leases onto the balance sheet, track Right-of-Use (ROU) assets, and produce ASC 842 disclosure reports.

But for hardware companies shifting to XaaS, you are now the Lessor. You are earning income, not incurring liabilities. That income must follow both ASC 842 (for the hardware) and ASC 606 (for the software/services).

This is where every lessee-focused product breaks; they’re focused on the lessee, not the lessor.

Today, most hardware CFOs are forced to address this with a patchwork of tools never designed for lessor revenue accounting. They attempt to stitch together:

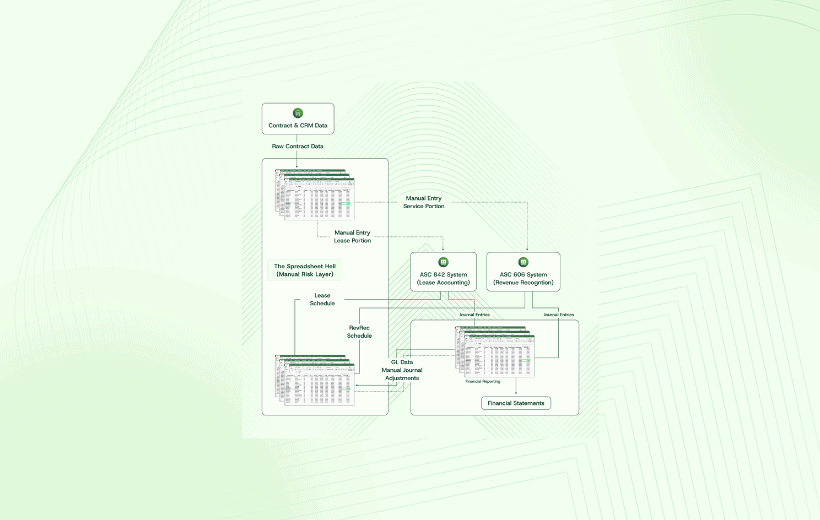

- Spreadsheets: The manual “glue” used to calculate allocations and track modifications outside the system.

- ERP-Native Modules: Oracle Lease Accounting, SAP RE-FX, or NetSuite Fixed Assets.

- Lessee-First Point Solutions: LeaseQuery (FinQuery), Visual Lease, Nakisa, EZLease, or MRI.

While these systems do a solid job helping lessees centralize expense contracts, they are architected as standalone lease subledgers. They sit outside of ASC 606 revenue systems, leaving the critical allocation and “Day 2” modification logic for your bundled contracts to be handled in spreadsheets. A dependence on spreadsheets is exactly where timing mismatches and audit comments tend to appear.

This guide compares the four primary approaches available to solve the XaaS lessor accounting problem.

Key Terminology for the XaaS Transition

Before evaluating software, it is critical to align your team on the specific terms that define your new accounting reality.

- Hybrid Contract: A single commercial agreement that contains both a lease component (the hardware/asset) and a non-lease component (software, maintenance, or managed services).

- Embedded Lease Arrangement: When a contract conveys the “right to control” the use of an identified asset for a period of time, even if the contract is legally labeled as a “Managed Services Agreement”. Under ASC 842, the hardware inside that service contract is a lease and must be separated.

- The “Synchronization Gap”: The structural compliance risk that occurs when Lease Income (ASC 842) and Revenue (ASC 606) are calculated in separate systems. When a contract is modified (e.g., an extension or upgrade), the two systems often fail to update simultaneously, creating material financial misstatements.

The 5 Fatal Flaws of Lessee Tools for XaaS

Why can’t you just use a standard lease accounting tool? Because they fail the “Lessor Model” required for modern XaaS.

- Lessee-First Design: Data models are optimized for expenses and liabilities, not lease receivables, net investment, or lease income across tens of thousands of devices.

- No Native ASC 606 Engine: They typically cannot run ASC 842 and ASC 606 together. They lack performance obligations and SSP libraries, forcing you to do the separation and allocation logic in Excel outside the system.

- Limited Support for High-Volume Portfolios: Many tools are designed around real estate portfolios with relatively few leases, not device fleets, IoT hardware, or embedded equipment programs with high transaction volumes.

- Failure of “Day 2” Modifications: When a contract changes (e.g., a term extension), lessee tools only adjust the liability. They lack the logic to re-allocate the revenue transaction price across the bundle. This forces manual recalculation and retrospective adjustments outside the system both of which are the primary sources of revenue leakage and restatements.

- Fragmented Audit Trail: Standard reports focus on lessee disclosures, not the full story of lease income, related service revenue, and how allocations changed over time.

The 4 Approaches to Lessor Accounting

Method 1: The “Patchwork” Approach (Spreadsheets + ERP/RevRec)

Common Stacks: Spreadsheets combined with SAP (Custom), Oracle RMCS, Zuora, or NetSuite ARM.

The Reality: Most companies do not run on spreadsheets alone. Instead, they use Excel as the “manual glue” to bridge the gap between their ERP (recording the lease receivable) and their Revenue Recognition system (recording the service revenue).

The Risk: This creates a disconnected workflow. When a contract “Day 2” modification occurs, such as a customer upgrading a device mid-term, finance teams must manually calculate the new allocation in Excel, then key the data into the ERP, and then key it again into the RevRec system. This manual triangulation is the primary source of material weaknesses in audits.

Method 2: The “Siloed” Approach (Legacy ERP Modules)

Vendors: SAP (RE-FX), Oracle (Lease Accounting), NetSuite (Fixed Assets/Lease).

The Reality: Major ERPs offer native lessor modules, but they were historically architected for Real Estate (buildings). More importantly, they are siloed from the ERP’s own revenue recognition engine.

The Risk: To make the Lease module talk to the Revenue module for a bundled contract, you effectively have to build your own software via brittle custom code.

Method 3: The “Operational” Approach (Point Solutions)

Vendors: Odessa, Solifi, NETSOL.

The Reality: These are the “Gold Standard” for managing the physical asset lifecycle, i.e. tracking insurance, credit scores, and repossession logistics.

The Risk: While these tools can handle a lease modification operationally (e.g., extending a contract term), they are “Revenue Blind”. They update the lease receivable but fail to trigger the required ASC 606 re-allocation for the bundled services. This leaves the revenue side of the house out of sync, requiring manual intervention to close the books.

Method 4: The “Unified” Approach (Lessor Subledger)

Vendors: RightRev.

The Reality: A Unified Subledger ingests the contract once and uses a single engine to automate both ASC 842 and ASC 606.

The Benefit: It eliminates the Synchronization Gap. When a contract is modified, the system automatically remeasures the lease and reallocates the revenue in lockstep, without spreadsheets.

The Vendor Landscape at a Glance

Below is a breakdown of key vendors, categorized by their architectural focus.

Category A: The Operational Specialists (Asset-First)

- Odessa: The “Gold Standard” for operational depth (repossession, credit), but “revenue blind” regarding ASC 606 bundles.

- Solifi (InfoLease): Industry standard for auto/heavy equipment finance, but lacks the integrated revenue recognition logic for XaaS bundles.

- NETSOL: Strong on full lifecycle workflow for traditional finance, but not built for converged software/hardware bundles.

The Verdict: These tools are excellent engines for your assets, but they are blind to your revenue. If you have a pure lending portfolio, they are perfect. If you have bundled services, they force you back into spreadsheets for the accounting.

Category B: The ERP “Native” Modules (The Silo Trap)

- SAP (RE-FX + RAR): Designed for Real Estate. Connecting RE-FX (Lease) to RAR (Revenue) typically requires “brittle custom ABAP code”.

- Oracle (Legacy OLFM & Cloud): Legacy OLFM is deep but siloed from modern Revenue Management (RMCS). The newer Cloud module is immature and property-focused.

- Netgain (NetLessor): Native NetSuite add-on. Good for simple leases but hits a “complexity ceiling” in high-volume scenarios due to reliance on NetSuite’s ARM.

The Verdict: Don’t let the “Native” label fool you. These modules are often just as siloed as a third-party tool, but come with a higher price tag for custom integration logic. They work best for real estate, not high-volume equipment bundles.

Category C: The Lessee-First Tools

- Visual Lease: A strong platform for real estate tenant compliance and administration, but it lacks the native revenue allocation engine required for hardware lessors to manage hybrid contracts.

- EZLease: An effective, simple solution for tracking lessee expenses, but it is not architected to handle the complex receivable tracking and revenue synchronization of a modern lessor.

- MRI Software: The industry standard for real estate property management, but its “building-centric” architecture is too rigid to handle the usage-based, serial-number-level complexity of equipment leasing.

- Nakisa: A powerful tool for global enterprises needing deep SAP integration, but its data model is heavily biased toward real estate, creating complexity for high-volume equipment revenue.

- LeaseQuery (FinQuery): The market leader for lessee expense compliance, but it is fundamentally designed to track liabilities (paying rent) and lacks the ASC 606 capabilities needed to recognize income (collecting rent).

The Verdict: These tools have done a solid job helping lessees centralize expense contracts. However, they are fundamentally Lessee-First. They lack the sophisticated revenue allocation engines needed to handle the income side of a hybrid XaaS contract.

Category D: The Unified Subledger

- RightRev: The only Unified Subledger that models the contract once to automate both ASC 842 and ASC 606 simultaneously. It ensures that any change to the lease term automatically triggers the correct revenue reallocation in real-time.

The Verdict: This is the only architecture purpose-built for the XaaS economy. By unifying the lease and revenue engines, it turns “Day 2” modifications from a material weakness risk into an automated non-event.

Summary: The XaaS Capability Matrix

| Methodology | Spreadsheets + ERP/RevRec | Legacy ERP (SAP/Oracle) | Ops Specialist (Odessa) | Unified Subledger (RightRev) |

| Core Architecture Focus | The “Glue” | General Ledger (GL) | Asset Lifecycle Management | Revenue & Leasing |

| Hybrid Contract Handling | Manual Calculation | Siloed (Custom Code) | Revenue Blind (Export) | Automated Allocation |

| Embedded Lease Support | Manual/Disconnected | Rigid (Real Estate Bias) | Lessee-Only (No Rev Rec Link) | Native / Event-Driven |

| “Day 2” Modification Risk | Material Weakness | High (Sync Failure) | Medium (Disconnected Workflow) | Eliminated |

Conclusion

Any solution that treats leasing and revenue as separate problems will inevitably push risk into spreadsheets, manual processes, and audit exposure. The unified subledger approach reflects a simple but critical reality: in XaaS, lease income and service revenue are economically inseparable, and your systems must treat them that way. As finance leaders evaluate their next phase of scale, the question to ask isn’t “Can this tool handle leases?” but “Can it keep my lease and revenue in sync automatically and as the business evolves?”

Ready to move beyond patchwork accounting?

When hardware, software, and services are sold together, revenue accuracy depends on more than compliance. It depends on architecture. RightRev consolidates lease and revenue accounting into a single, unified system so every contract modification is reflected correctly, in real time.

Get in touch to learn how RightRev serves as the accounting foundation for scalable XaaS monetization.

To learn more, join our January 22 webinar, The Lease Accounting Blind Spot: Understanding the Risks.